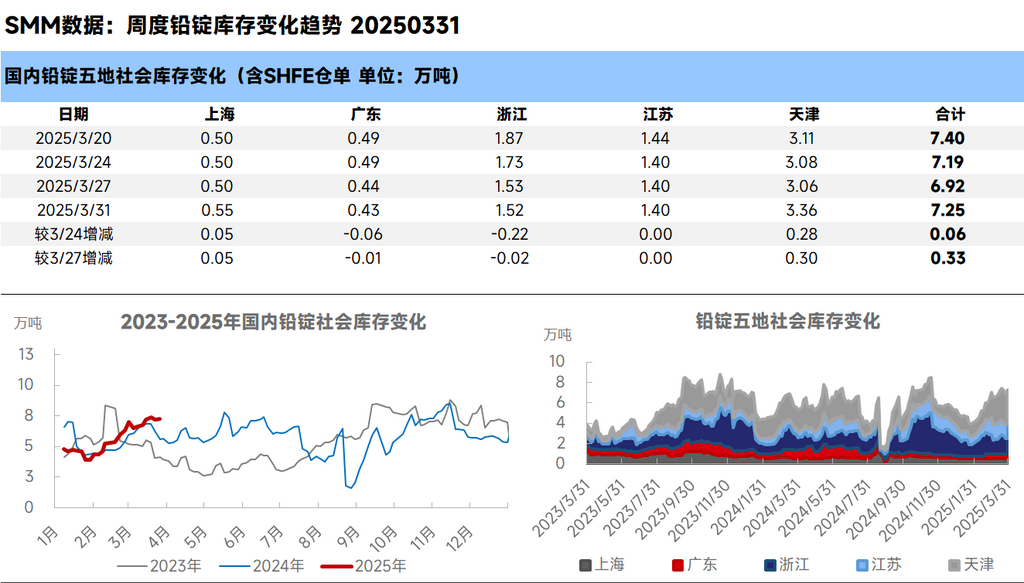

SMM March 31 News: According to SMM, as of March 31, the total social inventory of SMM lead ingots in five regions reached 72,500 mt, an increase of over 600 mt compared to March 24, and an increase of 3,300 mt compared to March 27.

Recently, both supply and demand in the lead market have declined. Due to factors such as routine maintenance and difficulties in scrap recycling, production at primary lead and secondary lead smelters has been reduced. As the traditional off-season for the lead-acid battery market approaches, downstream companies are cautious in production, with some cutting production or taking holidays. Meanwhile, after surging last week, lead prices pulled back, leading to a strong wait-and-see sentiment among downstream companies. Some even temporarily halted long-term contract purchases, resulting in a significant reduction in phased procurement. This has prompted suppliers to transfer lead ingots from in-plant inventory to social warehouses, pushing social inventory back above 70,000 mt. Additionally, after the decline in lead prices, profits from secondary lead quickly shrank, dampening production enthusiasm among some smelters. As April approaches, the delivery of the SHFE lead 2504 contract is on the agenda, with attention focused on the movement of delivery brand goods to delivery warehouses.